Introduction

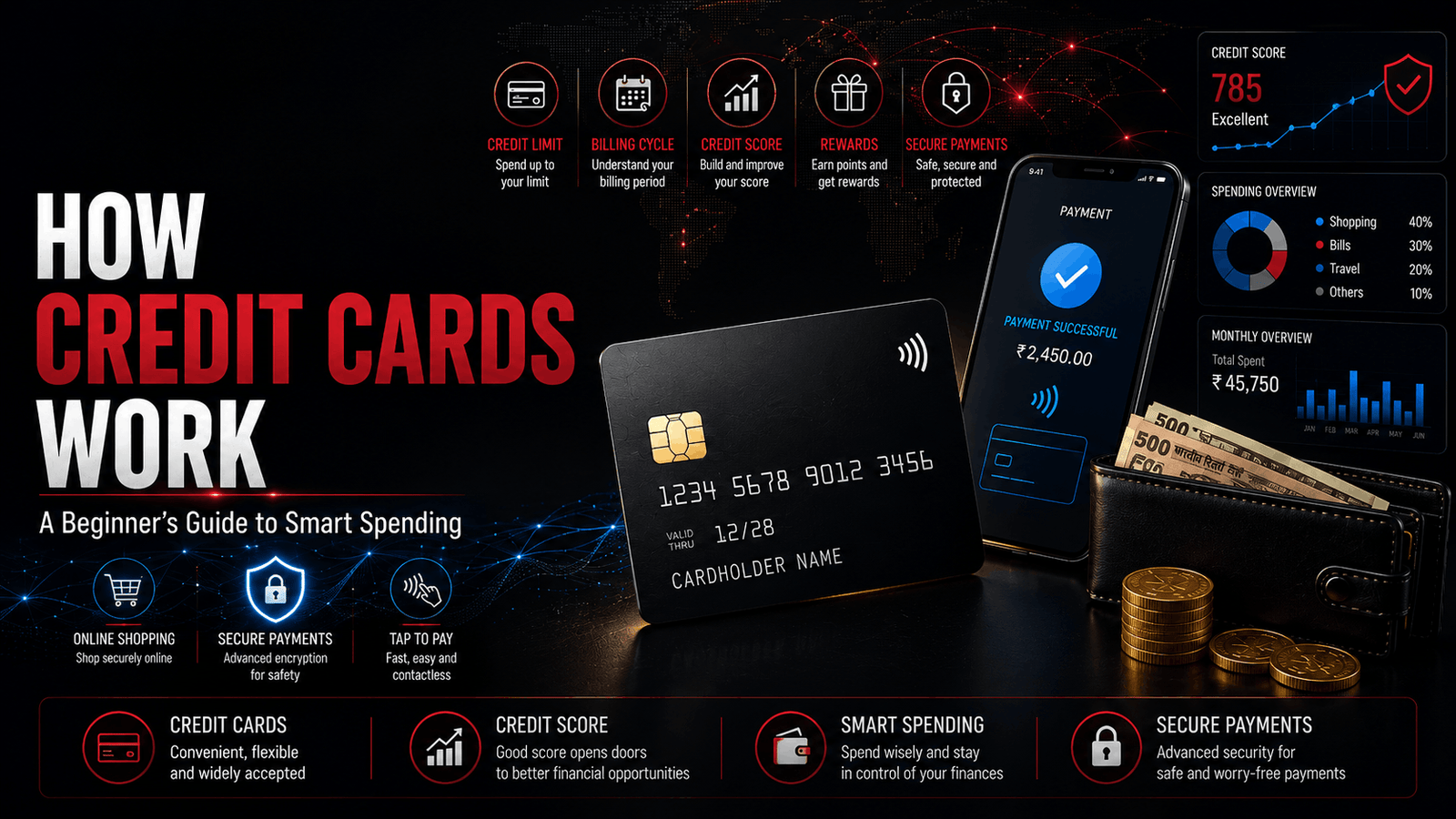

Credit cards are among the most misunderstood financial products.

Some people avoid them completely because they fear debt, while others use them without fully understanding how they work.

The truth is that a credit card isn't free money—it's a short-term loan from your bank or card issuer. When used responsibly, it can help you build a good credit history, earn rewards, and manage cash flow. Used carelessly, however, it can become expensive due to interest charges and late fees.

This guide explains everything in simple language.

What Is a Credit Card?

- Definition

- How it differs from a debit card

- Why banks issue credit cards

How Does a Credit Card Work?

Explain the entire process:

Customer purchases

↓

Bank pays merchant

↓

Customer receives bill

↓

Customer repays bank

Use a simple example with ₹10,000.

What Is a Credit Limit?

Explain:

- Initial limit

- How banks decide it

- Can it increase?

Understanding the Billing Cycle

Explain:

- Statement date

- Due date

- Interest-free period

Use a timeline example.

What Happens If You Pay the Full Amount?

- No interest

- Better credit history

- Reward points continue

What Happens If You Pay Only the Minimum Amount?

Explain:

- Interest starts

- Debt grows

- Long repayment period

Give an example.

Understanding Interest Rates

Explain APR.

Monthly interest.

Compound effect.

Simple examples.

Late Payment Charges

Explain:

- Late fee

- Interest

- Credit score impact

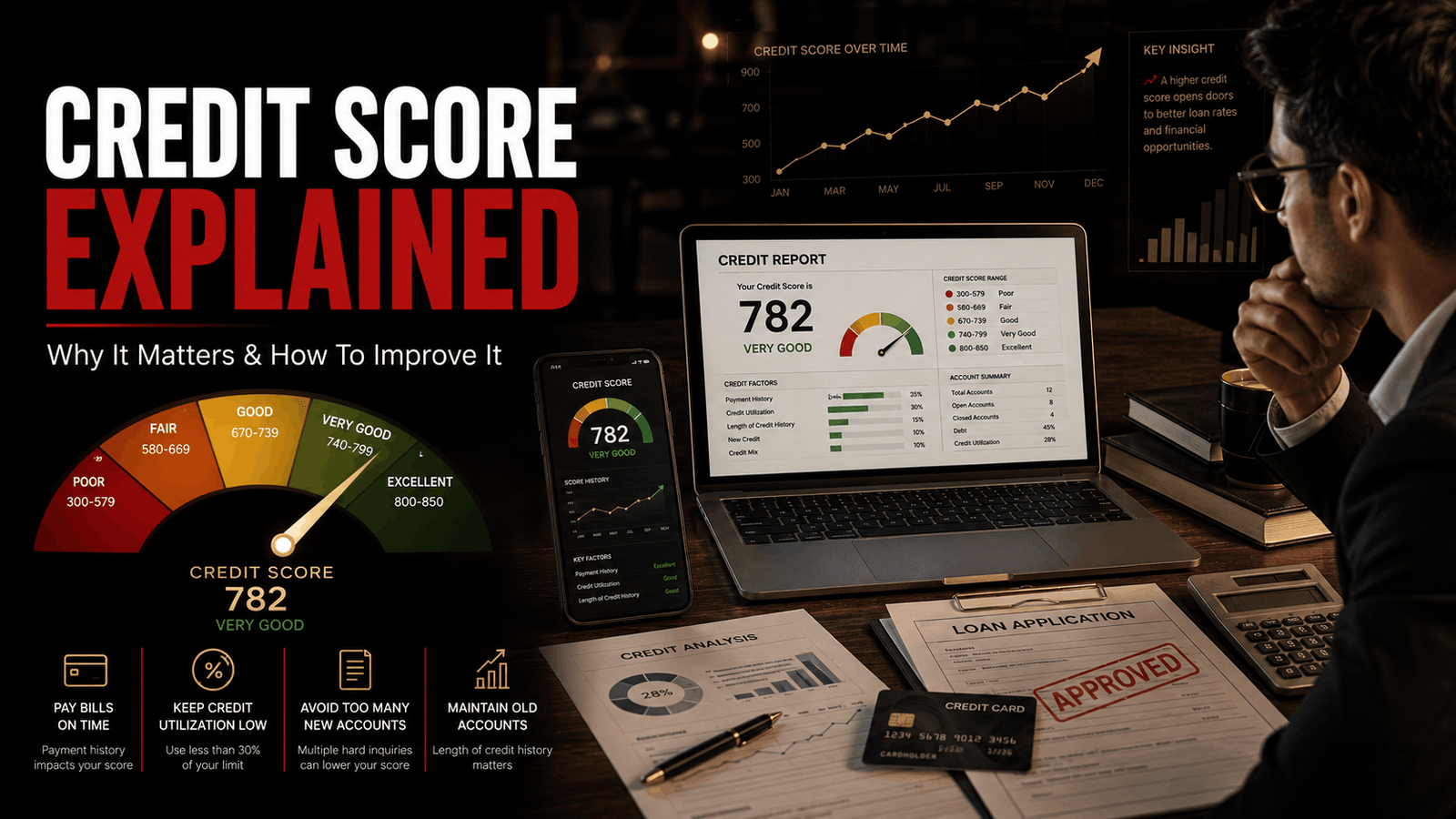

What Is a Credit Score?

Explain:

- CIBIL Score (India)

- Importance

- Loan approval

- Home loans

- Car loans

How to Build a Good Credit Score

- Pay on time

- Keep utilization below 30%

- Don't close old cards unnecessarily

- Avoid multiple applications

Credit Card Rewards

Explain:

- Cashback

- Reward points

- Airport lounge

- Travel miles

- Fuel benefits

Common Mistakes

❌ Paying minimum only

❌ Missing due date

❌ Cash withdrawal

❌ Overspending

❌ Using entire limit

Are Credit Cards Bad?

Balanced answer.

Advantages

Disadvantages

Tips for Beginners

Choose card wisely

Auto-pay

Track expenses

Pay in full

Don't buy what you can't afford

Blog of Time Insight

A credit card is neither good nor bad—it's a financial tool. Its value depends on how responsibly it is used. Paying the full statement balance on time and avoiding unnecessary debt can help you enjoy the benefits while minimizing the risks.

Key Takeaways

✅ Credit cards are short-term borrowing tools.

✅ Paying the full bill usually avoids interest.

✅ Timely payments help build a good credit history.

✅ Using only a portion of your available limit is generally considered healthier for your credit profile.

✅ Responsible spending matters more than having multiple cards.

Future Outlook

Discuss:

- Virtual Credit Cards

- AI Fraud Detection

- Contactless Payments

- Digital Wallets

- Buy Now, Pay Later (BNPL)

- Tokenization

- Future of cashless payments

📌 Conclusion

Credit cards can simplify payments, improve financial flexibility, and help build a strong credit profile when used wisely. Understanding how billing cycles, interest, and repayment work is the first step toward making informed financial decisions. The best habit is simple: spend within your means and pay your statement balance in full whenever possible.